The Hidden Price Tag on Your Prescription

You walk into the pharmacy, hand over your script, and wait for the total. That number isn't just the price of the medicine. It's a complex calculation based on where your drug sits in your insurance plan's hierarchy. In 2024, this hierarchy-specifically the difference between generic copays and the higher cost-sharing amounts required for brand-name medications-determined whether millions of Americans could afford their daily health maintenance.

If you are trying to understand why one pill costs $5 and another looks like a mortgage payment, you are looking at the tiered formulary system. This system was designed to nudge patients toward cheaper alternatives while keeping expensive treatments accessible. But "accessible" doesn't always mean "affordable." Let's break down exactly what these numbers looked like in 2024, how they impacted your wallet, and what changed with the new regulations.

How Insurance Tiers Dictate Your Cost

To understand the cost, you first need to understand the structure. Most health plans, including Medicare Part D and commercial health insurance programs that cover prescription drugs, use a four or five-tier system. Think of it like airline seating: economy is cheap but basic; first class is expensive but offers more perks (or in this case, specific chemical formulations).

- Tier 1 (Preferred Generic): These are the cheapest options. They are widely available and heavily negotiated by insurers.

- Tier 2 (Non-Preferred Generic): Still generic, but perhaps from a less common manufacturer or not prioritized by your specific plan.

- Tier 3 (Preferred Brand): Brand-name drugs that your insurer considers standard care for certain conditions.

- Tier 4 (Non-Preferred Brand): Expensive brand-name drugs, often newer or with no generic equivalent yet.

- Tier 5 (Specialty): High-cost drugs for complex conditions like cancer or rheumatoid arthritis.

Your copay is fixed based on which tier your doctor prescribes. If your doctor writes for a Tier 1 drug, you pay the Tier 1 rate. If they write for a Tier 3 drug, you pay the Tier 3 rate. The gap between these tiers is where the financial stress happens.

Average Generic Copays in 2024

For most people, generics were the financial anchor of their healthcare budget. In 2024, the trend continued toward lower costs for these essential medicines. According to data from the Centers for Medicare & Medicaid Services (CMS) and analyses by the Kaiser Family Foundation (KFF), the median copay for preferred generic drugs in Medicare Advantage plans hovered around $4 to $7.

However, "median" hides some reality. Many large commercial plans and aggressive Medicare Advantage plans offered $0 copays for Tier 1 generics to attract enrollees. If you had Extra Help (Low-Income Subsidy) through Social Security, your cap was strictly enforced at $4.50 for generics.

Why so low? Because generics make up about 92% of all prescriptions filled in the U.S., according to IQVIA data. Insurers absorb the small loss on a $5 copay because it prevents you from skipping doses or seeking cash prices elsewhere. It’s a volume game.

The Steep Climb of Brand Name Copays

Now, let’s talk about the brand names. This is where the math gets painful. In 2024, if you needed a preferred brand-name drug (Tier 3), the median copay for Medicare Advantage enrollees was approximately $47. For non-preferred brands (Tier 4), that median jumped to $100 per prescription.

But here is the trap: many standalone Prescription Drug Plans (PDPs) did not use fixed copays for brands. Instead, they used coinsurance. This means you paid a percentage of the drug's actual cost. If a brand drug costs $300 and your coinsurance is 20%, you pay $60. If the drug costs $1,000, you pay $200. There was no ceiling until you hit the catastrophic coverage phase.

KFF analysis showed that 89% of PDP enrollees faced this coinsurance model for preferred brands, compared to only 3% in Medicare Advantage plans. This created a massive disparity in predictability. MA-PD users knew exactly what they would pay ($47). PDP users had to check the invoice every time.

| Drug Tier | Medicare Advantage (MA-PD) | Standalone PDP | Commercial Insurance (Typical) |

|---|---|---|---|

| Preferred Generic (Tier 1) | $0 - $7 (Fixed) | $0 - $10 (Fixed) | $10 - $30 (Fixed) |

| Preferred Brand (Tier 3) | $47 (Median Fixed) | 22% Coinsurance | 20-30% Coinsurance |

| Non-Preferred Brand (Tier 4) | $100 (Median Fixed) | 47% Coinsurance | 40-50% Coinsurance |

| Specialty (Tier 5) | $150+ or % | High % Coinsurance | Case-by-case |

Why Did My Doctor Prescribe the Expensive One?

If generics are so cheap, why do doctors still prescribe brands? You might hear the phrase "dispense as written" on your label. This usually happens for three reasons:

- Biological Differences: Some drugs, like those for epilepsy or thyroid issues, have a narrow therapeutic index. A slight variation in the generic manufacturing process can cause side effects or reduced efficacy. Doctors stick to the brand to ensure consistency.

- Patient History: If you tried the generic last year and got headaches, your doctor will likely switch back to the brand. Your body knows the difference.

- No Generic Available: Sometimes patents haven't expired yet, or the generic market is unstable due to supply chain issues.

However, there is a fourth reason: inertia. Sometimes, a doctor simply hasn't updated their prescribing habits. If you are paying a high brand copay, ask your pharmacist: "Is there a therapeutic alternative on a lower tier?" Often, there is a different brand or a generic that works just as well.

The "Member Pays the Difference" Trap

This is the most confusing part of 2024's landscape. Many commercial plans and some Medicare plans implemented a policy called "Member Pay the Difference." Here is how it kills your budget:

Imagine a generic statin costs $10. The brand name version costs $100. Your plan has a $20 copay for brands. You think, "I'll just pay $20." Wrong. Under this policy, you pay the brand copay ($20) PLUS the difference in acquisition cost ($90). Total bill: $110.

This policy is designed to force you to take the generic. If your doctor insists on the brand, you bear the full brunt of the price gap. Always check your plan's Summary of Benefits for this clause. It turns a manageable copay into a shock.

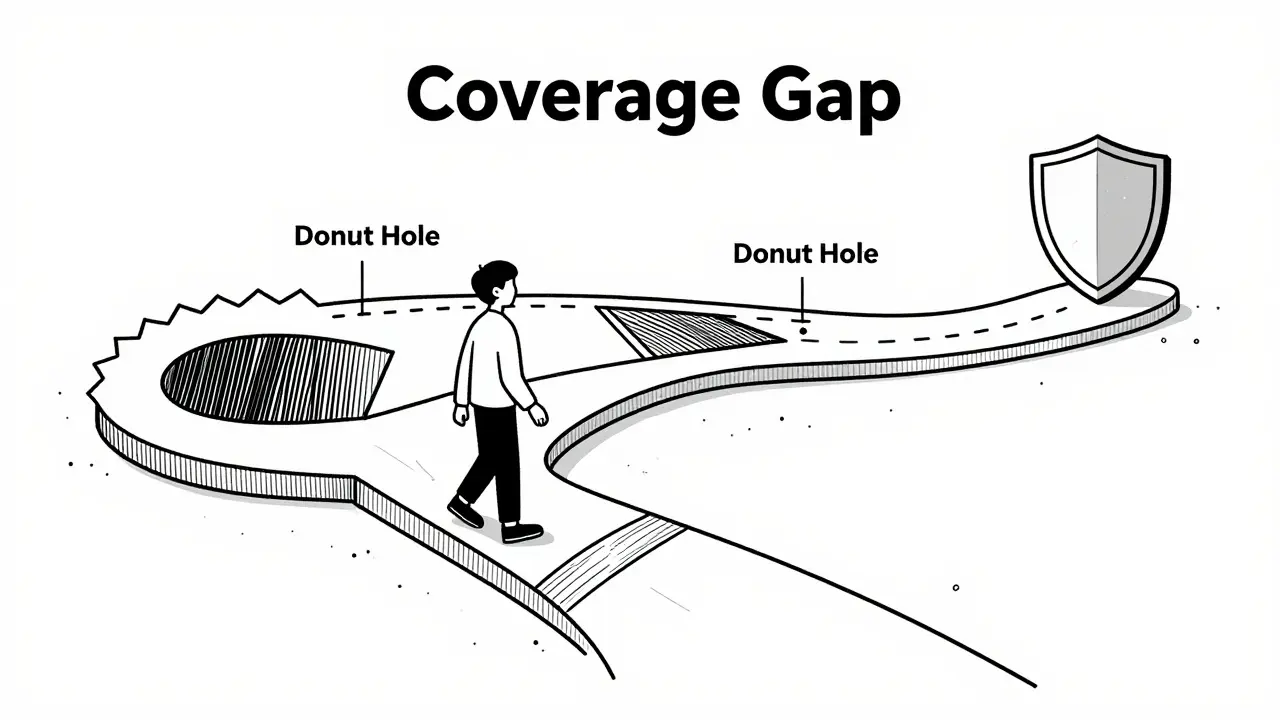

Navigating the Coverage Gap

In 2024, the "donut hole" was technically closed, but the coverage phases still mattered. Once your total drug costs (what you paid + what insurance paid) hit $1,700, you entered the Coverage Gap. During this phase, you paid 25% of the cost for both brand and generic drugs until you hit $8,000 in total spending.

After $8,000, you entered Catastrophic Coverage. Here, you paid either 5% coinsurance or a small copay, whichever was greater. For brand-name users, this phase was crucial. Without it, a single month of specialty drugs could wipe out savings. The Inflation Reduction Act capped this liability, ensuring that even heavy brand users had a safety net, though reaching that cap required significant upfront spending.

Strategies to Lower Your Out-of-Pocket Costs

You don't have to accept the sticker price. Here are practical steps to reduce your burden:

- Use the Plan Finder Tool: Before enrolling (or during Open Enrollment), plug your specific meds into the CMS Plan Finder. Don't look at monthly premiums alone. Look at the projected annual out-of-pocket cost for your specific list.

- Ask for Prior Authorization Waivers: If your doctor needs a brand, ask them to submit a "medical necessity" letter. This can sometimes move a Tier 4 drug to Tier 3 pricing.

- Check for Patient Assistance Programs (PAPs): Pharmaceutical companies offer PAPs for uninsured or underinsured patients. Even if you have insurance, some programs help bridge the gap if your income qualifies.

- Consider Mail-Order Pharmacies: For 90-day supplies of maintenance drugs (like blood pressure or cholesterol meds), mail-order pharmacies often offer lower copays than retail counters. Many plans incentivize this with a discounted rate.

- Review Quarterly: Formularies change. A drug that was Tier 2 in January might be Tier 4 in July. Check your formulary updates regularly.

What Changed in 2025 and Beyond

While we are analyzing 2024 costs, it is vital to know that the landscape shifted dramatically starting in 2025. The Inflation Reduction Act introduced a hard $2,000 annual out-of-pocket maximum for Medicare Part D beneficiaries. This means no matter how many brand-name drugs you take, once you spend $2,000, the insurance pays 100% for the rest of the year.

Additionally, the insulin cap remained at $35/month. For diabetics, this removed a major variable. However, for those on other specialty brands, the $2,000 cap is a lifeline that didn't exist in previous decades. If you are planning for next year, expect fewer surprises, but also potentially higher initial copays as insurers adjust to the new risk pool.

What is the average generic copay in 2024?

The average generic copay for preferred generics in Medicare Advantage plans ranged from $0 to $7. For those with Extra Help, the maximum was $4.50. Commercial plans typically charged between $10 and $30 for Tier 1 generics.

Why is my brand name copay so much higher than the generic?

Brand name drugs are placed on higher tiers (Tier 3 or 4) because they cost the manufacturer more to produce and market. Insurers charge higher copays to discourage use unless medically necessary. In 2024, the median brand copay was $47 for preferred brands and $100 for non-preferred brands in Medicare Advantage plans.

What does "Member Pay the Difference" mean?

This policy requires you to pay your standard brand copay plus the additional cost difference between the brand drug and the generic alternative. For example, if the generic is $10 and the brand is $100, and your copay is $20, you might pay $110 total ($20 copay + $90 difference).

Do I have to pay coinsurance for brand drugs?

It depends on your plan type. Most Medicare Advantage (MA-PD) plans use fixed copays (e.g., $47). However, most standalone Prescription Drug Plans (PDPs) use coinsurance, meaning you pay a percentage of the drug's cost (e.g., 20-25%). Coinsurance can lead to unpredictable bills for expensive drugs.

How can I find out if my drug is covered?

You should check your plan's Formulary, which is a list of covered drugs. This document is updated annually and must be provided by your insurer. You can also use the Medicare Plan Finder tool online to enter your medications and see their tier status across different plans.

Is there a cap on how much I pay for drugs?

In 2024, there was no hard annual cap for most beneficiaries, though catastrophic coverage kicked in after $8,000 in total drug costs. Starting in 2025, the Inflation Reduction Act imposes a $2,000 annual out-of-pocket maximum for Medicare Part D enrollees.